Milk and Memory Chips

In March 2026, British dairy farmers were pouring milk down the drain. That same month, memory chip stocks lost $100 billion in market value.

One is an agricultural commodity crisis. The other is a technology repricing driven by a Google Research paper. They share no supply chain, no customer base, no geography. But they share a structure: in both cases, productivity outran the infrastructure meant to absorb it.

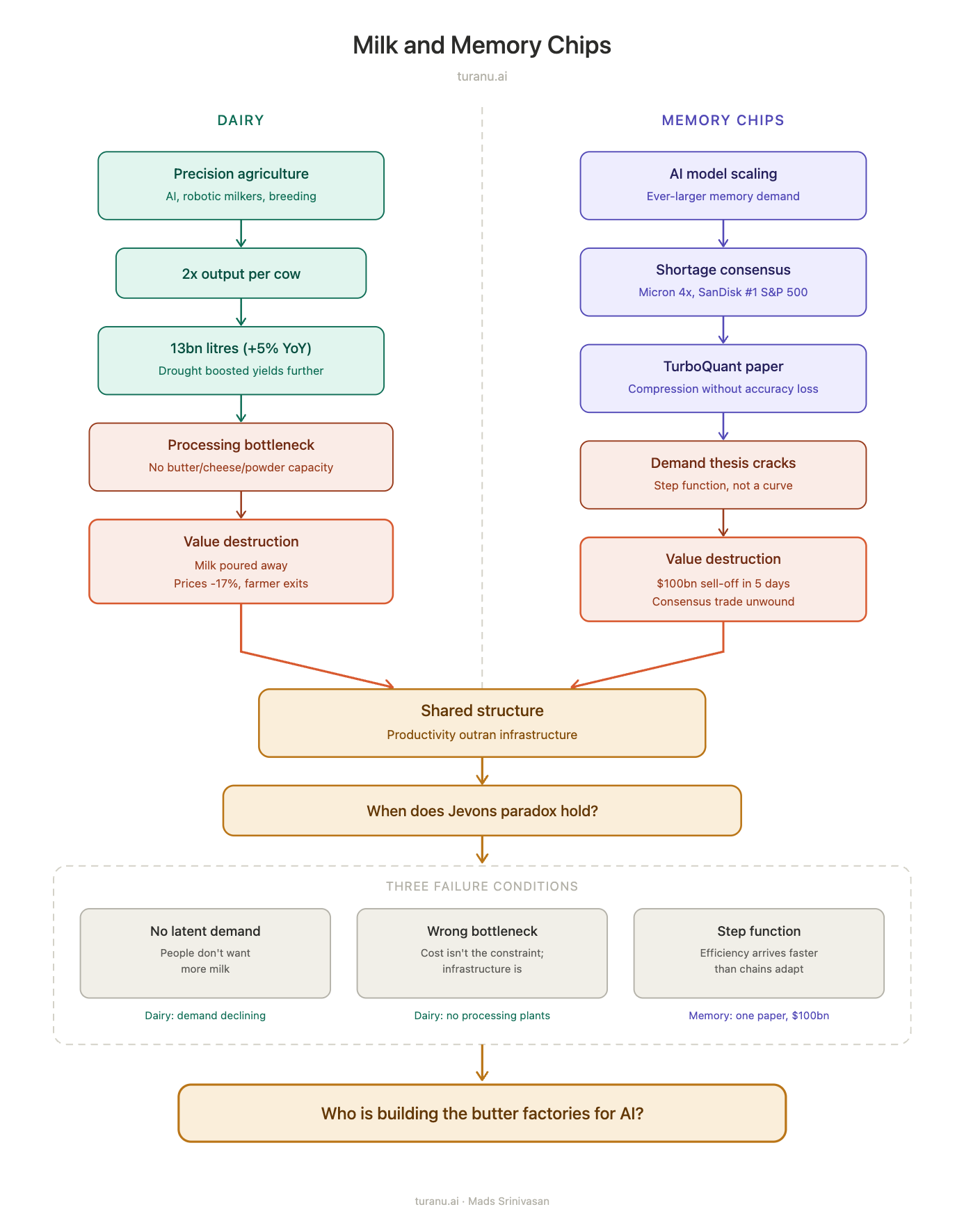

Britain's dairy herd is the smallest it has been in decades. But output hit 13 billion litres this year, up 5% over 2024. A modern British cow produces twice the milk of a 1970s cow: robotic milkers, wearable health monitors, AI-optimized breeding, precision feed management. A drought last summer forced farmers onto nutrient-rich winter feed earlier than usual, accidentally boosting yields further. The cows have never been more productive.

The problem is downstream. Britain doesn't have enough processing plants to convert surplus raw milk into butter, cheese, or powder. The Netherlands and New Zealand can absorb production swings because they built that capacity. Britain didn't. So when output surges, the milk gets poured away. Not because nobody wants it: British dairy exports hit a record £2.2 billion last year. But because the infrastructure between the cow and the customer doesn't exist at the scale the cow now demands.

Prices dropped 17% since September. Farmers are selling below production cost. A Cheshire farm lost £20,000 a month in revenue between September and February. The herd keeps shrinking: down 20% since 2019, to roughly 7,000 farms. The ones that survive will be larger, more automated, more productive. Which will produce more milk. Which will need more processing capacity that still won't be there.

Meanwhile, in a different commodity market: memory chips.

The memory chip shortage was Wall Street's favorite AI trade for 2025 and into 2026. The logic was simple: AI models need enormous amounts of high-bandwidth memory; supply is constrained; prices go up; Micron, SanDisk, and SK Hynix print money. Micron's market cap quadrupled in a year. SanDisk was the best-performing stock in the S&P 500 in 2025. The shortage was real enough that Sony announced PS5 price increases of up to 20%, partly driven by memory component costs.

Then Google Research published TurboQuant, a model compression algorithm that promises to run AI models on dramatically less memory without accuracy loss. In five days, memory stocks shed $100 billion. Micron dropped 15%. The consensus trade cracked.

Morgan Stanley's defense was immediate and textbook: Jevons paradox. If models need less memory per query, inference costs drop, more people deploy AI, total demand grows, and memory makers are fine. This is the standard efficiency-expands-demand argument, and it has centuries of economic history behind it. When engines got more fuel-efficient, people drove more. When lighting got cheaper, cities used more of it. Efficiency doesn't reduce demand; it unlocks it.

Except when it doesn't.

British dairy farmers doubled their output per cow over 50 years. Demand didn't double. It shrank. Fewer people eat cereal. Plant-based alternatives are growing. Dietary patterns shifted. The efficiency gains are real and structural; the demand expansion that Jevons predicts never materialized. Instead, the productivity just created surplus that the system couldn't absorb.

Morgan Stanley's note assumes the answer. The conditions are worth examining.

Three conditions are required, and all three can fail:

First, latent demand must exist. Jevons works when there are people who want the thing but can't afford it yet. AI probably has this: millions of enterprises that would deploy models if inference were cheaper. Dairy doesn't: people aren't drinking less milk because it's expensive. They're drinking less milk because they don't want milk.

Second, the bottleneck must be cost, not infrastructure. Cheaper AI inference only expands demand if the deployment infrastructure exists: compliance frameworks, integration layers, trust mechanisms, monitoring systems. If the bottleneck is regulatory approval or organizational readiness rather than compute cost, efficiency gains don't unlock anything. They just make the unused capacity cheaper. Britain has world-class cows and record export demand; it doesn't have the processing plants. The bottleneck isn't the cow.

Third, the efficiency gain must be gradual enough for the value chain to adapt. A research paper that compresses memory requirements by a significant fraction overnight is a step function, not a curve. Markets can adjust to curves. Step functions cause $100 billion in value destruction in a week. The dairy equivalent: a drought forcing an entire national herd onto winter feed simultaneously, creating a supply spike that the processing infrastructure was never sized to handle.

The pattern is the same in both cases: production capability advanced faster than the downstream system designed to capture its value. Britain built the world's most productive dairy herd and forgot to build the factories. The AI hardware trade priced in insatiable demand for memory and didn't price in that a single research paper could compress what the models actually need.

Every litre of milk poured down a drain is a failure of capital allocation, not agriculture. Every dollar of that $100 billion sell-off is a repricing of where the bottleneck actually sits: not in production, but in the infrastructure between production and value.

The dairy industry's version of this problem is visible and physical: milk on the ground, empty processing plants, farmers exiting the industry. The AI version is financial and abstract: compressed models, stranded capex assumptions, inference economics that shift faster than procurement cycles.

But the structural question is identical. And it applies to every technology cycle where capability outruns deployment: who builds the infrastructure that converts raw productive capacity into value? Who captures the margin between what the system can produce and what the market can absorb?

Britain doesn't need more cows. It needs butter factories. AI may not need more chips. It may need the deployment infrastructure that turns raw capability into value.

Who is building it?