Which SaaS Survives the Vibe-Coding Era?

The S&P 500 software sub-index is down 27% since October. Private equity firms are tripping over each other to downplay their software exposure. The Economist reports $500 billion in software-linked debt lurking in US credit markets. And "SaaS is dead" is having its moment as a LinkedIn hot take.

But "SaaS is dead" is wrong. It's too broad. The interesting question isn't whether software companies are in trouble. It's which ones, and why. More importantly: what can be done about it?

Two forces are converging that make this moment different from a normal correction. On the supply side, the cost of building custom software is collapsing for technically literate users. On the demand side, SaaS vendors are raising prices at 5x general inflation while bundling AI features many customers didn't ask for. The squeeze is real, but it's not squeezing everything equally.

The supply side: building got cheap

A year ago, replacing a SaaS product meant hiring developers or spending months on a side project. Today, a product manager with Claude or Cursor can prototype a functional replacement for many tools in an afternoon. Whether that prototype becomes a production tool depends on the complexity, but the fact that the question is even worth asking is what's changed.

This isn't theoretical. Netlify's CEO has said his employees built internal AI replacements for SaaS products like survey and quoting tools. Martin Casado, a partner at Andreessen Horowitz, built a personal CRM with AI because it was easier than learning a complex off-the-shelf product. Salesforce, the leading CRM vendor, has lost nearly half its value since early 2025. StackBlitz CEO Eric Simons put it bluntly: "There are many SaaS vendors we would have likely previously used that are no longer relevant."

These aren't fringe experimenters. They're CEOs and VCs choosing to build rather than buy, not because they enjoy coding, but because the off-the-shelf product was harder to use than prompting an LLM.

The demand side: SaaS got expensive

While building alternatives got cheaper, SaaS got more extractive. According to the Vertice SaaS Inflation Index, SaaS pricing is up 12.2% year over year, more than four times the 2.7% G7 inflation rate. Businesses now spend an average of $7,900 per employee annually on SaaS tools, up 27% in two years.

The price increases aren't subtle. Salesforce pushed through a 6% increase on Enterprise and Unlimited editions, and up to 72% of its go-forward revenue growth now comes from price increases rather than new customers. Slack jumped 20%. Adobe rebranded Creative Cloud as "Creative Cloud Pro," added AI features, and raised the price 17%. Microsoft added a 5% surcharge for choosing monthly billing over annual.

Meanwhile, roughly half of all SaaS licenses sit unused for 90 days or more. Companies are paying more for software they're not even using.

The macro picture compounds the pressure. The average company runs 275 SaaS applications. IT budgets grow at 2.8% annually. SaaS vendors raise prices at 9-25%. That math breaks eventually. For a growing number of technically capable teams, "eventually" arrived when they discovered they could vibe-code a replacement during a lunch break.

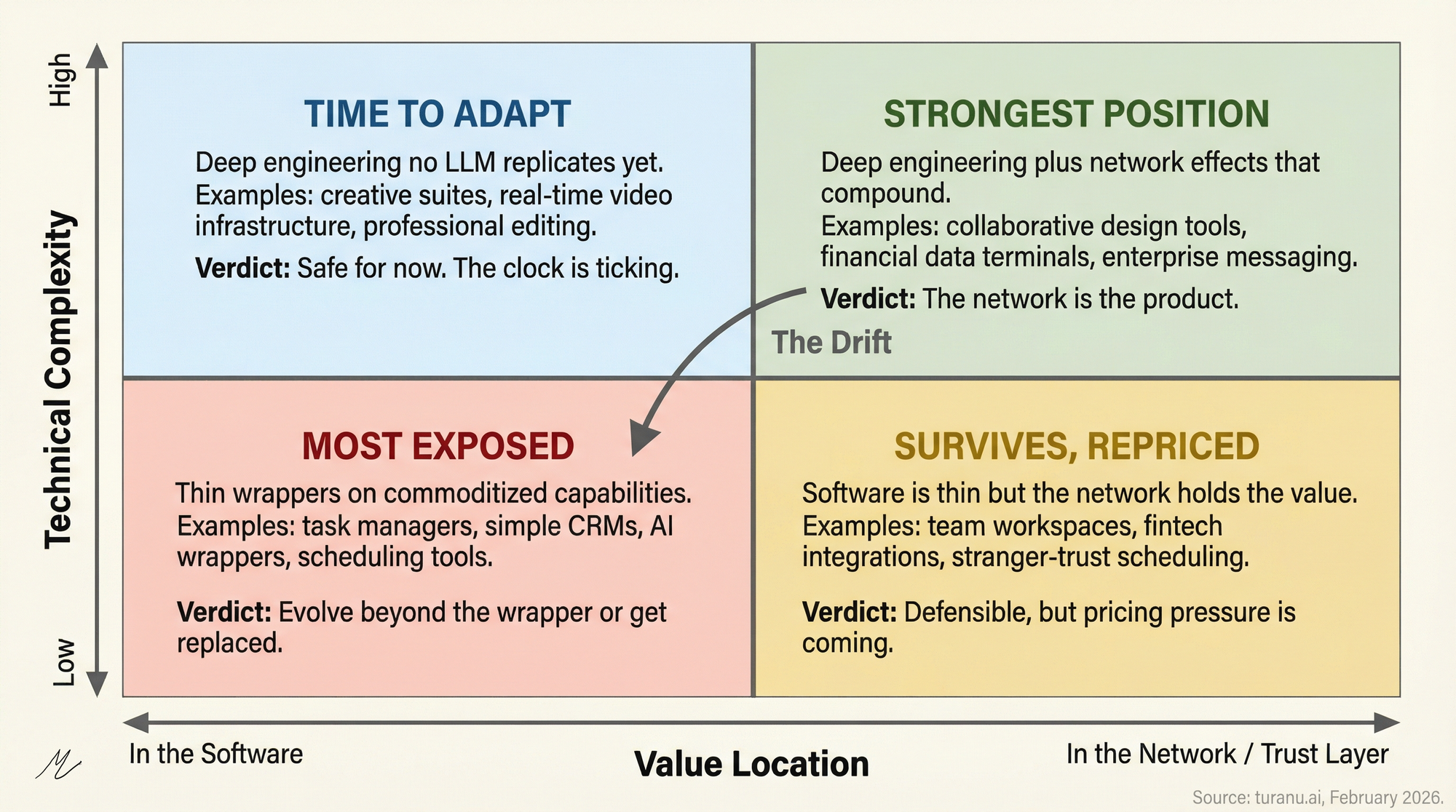

The framework: what's exposed and what isn't

Not all SaaS is equally exposed. The vulnerability depends on two dimensions: how technically complex the product is to replicate, and where the actual value lives.

Low complexity, value in the software itself. This is the most exposed quadrant. Task managers, scheduling tools, simple CRMs, AI image generation wrappers. These products started as thin UI layers over capabilities that are now commoditized. When Zapier is an if-then workflow you can describe in natural language, the subscription starts looking less like value and more like convenience. Some companies in this quadrant already see the shift. Grammarly has been expanding into broader writing workflows. Zapier has been investing heavily in AI-native automation, racing to move their value beyond what users can now build themselves. The playbook for this quadrant is clear: evolve the product beyond the wrapper, or watch your customers build their own.

Low complexity, value in the network or trust layer. Notion for teams, bank-connected budgeting apps, Calendly's stranger-trust factor. The software itself is replaceable, but the value extends beyond the code. Plaid integrations, shared workspaces, the fact that your client trusts a Calendly link more than a custom scheduling page. These products survive, but the pricing conversation is changing. Users increasingly understand how thin the software layer is, and they'll expect pricing to reflect where the real value lives: in the network, not the code.

High complexity, value in the software. Adobe's creative suite, Zoom's real-time video infrastructure, professional video editing. These represent years of deep engineering that no one is replicating in a weekend. The moat is genuine technical achievement, not a UI wrapper. Products in this quadrant have the most time to adapt, though they'll face pressure eventually as AI capabilities mature.

High complexity, value in the network. Slack, Figma, Bloomberg terminals. The strongest position. Deep engineering plus a network effect that compounds with every user. Traders still rely on Bloomberg terminals despite decades of attempts to create replacements. The network is the product. You could build a better terminal; you can't build the network that makes it indispensable.

The exposed quadrant is growing, but so are the escape routes

Here's what most "SaaS is dead" takes miss: the quadrants aren't static. Every improvement in AI capabilities slides products from the defensible quadrants toward the exposed one.

Consider CRM. Five years ago, Salesforce sat firmly in the high-complexity column. The customization engine, the app ecosystem, the integration layer represented genuine technical depth. Today, Casado built a personal CRM with a prompt. For a solo user or small team, the complexity moat has evaporated. Salesforce still dominates enterprise, but the bottom of their market is exposed in a way it wasn't two years ago.

The same erosion is happening in business intelligence, basic data analytics, project management, and customer support tooling. AlixPartners describes mid-sized SaaS companies as being squeezed between AI-native startups and tech giants bundling AI into existing platforms.

Anthropic's Cowork marked a step change here. Instead of answering questions, it plans and executes multi-step tasks: cleaning documents, building spreadsheets, analyzing data, automating workflows. Barclays analysts described it as closer to what Microsoft originally envisioned for Copilot, but with far greater autonomy. When a non-technical marketer can direct an AI agent in plain English to do what previously required a dedicated SaaS tool, the tool's value proposition needs to rest on something beyond the feature set.

But the quadrant borders move in both directions. The smart incumbents are investing in network effects, proprietary data layers, and ecosystem integrations that vibe-coded alternatives can't replicate. Salesforce's Agentforce is a bet that their data network and enterprise relationships matter more than the CRM features. Zapier's AI-native workflows are a bet that orchestration across hundreds of integrations is harder to replicate than a single automation. The companies moving fastest to anchor their value outside the software layer are the ones most likely to survive this transition.

What this means

The $7,900 per employee that companies spend annually on SaaS isn't going to zero. But a meaningful fraction of it sits in the exposed quadrant, and every quarter, that fraction grows. The software sell-off isn't irrational panic. It's the market trying to figure out which revenue streams are durable and which are sitting on a foundation that's shifting.

For product leaders evaluating their SaaS portfolio: map your tools against the two dimensions. Where is the value, really? In the software, or in what surrounds it? If a technically capable team member could replicate the core functionality in a day with an LLM, that's a signal to renegotiate, consolidate, or explore alternatives.

For founders building SaaS: the era of charging subscription fees for thin wrappers is ending. But this isn't a death sentence. It's a forcing function. The products that thrive will be the ones that move their value to where vibe coding can't follow: into the network, the data, the trust layer, or the deep engineering that an afternoon with an LLM can't touch, at least for now. The window to make that move is open, but it's narrowing.

That's the part I keep turning over. The "SaaS is dead" narrative frames this as a technology story. It's actually a value-location story. The technology just made it possible to test where the value really lives. Companies that understand the distinction have a path forward. The ones that don't are about to discover their moat was convenience, not capability.